Shutters and burglaries, Airbnb controls: Five French property updates

We also look into one city in Brittany’s fight to reduce Airbnb rentals, a landlord’s dispute with an elderly care association and the costs of home extensions

In this week’s roundup we are covering an insurance claim after a break in, mortgage refusal rates, Saint-Malo’s fight against Airbnb and the cost of home extensionsLIGHTITUP, Antoine2K, Craig Russell, Elle Aon / Shutterstock

Couple wins €52,000 insurance claim for theft despite leaving shutters open while away

An insurance company has been ordered to pay out €52,000 to a French couple to cover the cost of valuable jewellery stolen during a burglary at their home in 2015, despite the fact that they left the bedroom shutters open, a factor that usually means insurers are not responsible.

This is because of a clause within a clause of the contract that states that if the shutters would have had no effect on the outcome of the burglary, then the policy holders are not at fault and the insurance company must pay out.

How did the theft happen?

The couple went on a three-day trip in February but left the shutters covering their bedroom window open – the window was locked. They kept valuable jewellery in their bedroom in a safe.

The burglars climbed onto the balcony, broke a window, unlocked the French window doors from the inside and then proceeded to drill open the safe, which was fixed to the floor in a cupboard. They then took off with the jewellery .

How did the couple react?

They filed a complaint with the local gendarmerie and asked their insurer, Caisse régionale d’assurances mutuelles agricoles (Crama), for €70,000 in compensation. The insurer valued the stolen items at €52,000 but refused to pay out.

This is because the shutters had been left open.

Ad

The case went to court.

Results of the first court case

The judges at the High Court of Rennes ruled that a clause within the clause about the shutters meant that the couple were within their right to claim compensation.

Normally, stolen items are not covered “if there is a failure to observe preventive measures”, such as closing the shutters.

But the judges found that within the contract it stipulated that this is overruled if “the failure to comply with these measures would not have had any impact on the outcome of the theft or damage”.

The judges cited the “determination” of the burglars and their willingness to break open the safe as evidence that they would have been able to force open the shutters even if they had been closed.

The court ordered Crama to pay the couple the €52,000 in compensation on July 3, 2019.

Second court case

However, Crama appealed and the case went to court again on March 2 of this year.

This time, the couple themselves put forward the argument that the burglars would have been able to break in regardless of the shutters being closed.

The court ruled in their favour and Crama was ordered to pay the compensation.

Read our archive articles on handling burglaries and home insurance in France below:

Saint-Malo’s anti-Airbnb measures ‘starting to have effect’

The mayor of Saint-Malo (Ille-et-Vilaine) is cautiously optimistic that the measures to limit short-term holiday rentals in the city, introduced in June last year, are starting to have a positive effect.

Gilles Lurton decided to clamp down on the number of holiday lets, notably Airbnb lets, as locals were struggling to find housing and young people were being forced to move away.

“It is still too early to have precise information but the notaires tell us that they are observing a resumption of house sales and rentals to permanent residents,” Mr Lurton said.

“They can feel the trend shifting without being able to quantify it yet.”

Since last year, if a landlord wants to rent out a flat short term to tourists, they must make a demand for a “change in use” of the property, which serves as a type of holiday let permit.

The mayor introduced caps that cannot be exceeded on how many holiday lets are permitted within different areas of the city. If a landlord wants to change the use of their property to being a holiday let, they have to wait for a space to free up, which can happen when another landlord changes the usage of their property.

There are now 371 properties on the waiting list to become holiday lets in the city, including 63 in the area inside the granite walls that surround the old town.

But not everyone is happy. For the past 20 years, until last year, Sylvie Mitteaux-Martin rented out four properties to tourists during the summer months and to university students the rest of the year.

She has now had to give that up due to the limits. The retiree, who says she earns €960 per month from her pension, estimates that she is missing out on around €20,000, France 3 reports.

She and other unhappy landlords have launched legal action against the mairie for the measures, which they judge to be illegal.

Almost half of mortgage applications refused this year

Almost half of all mortgage applications have been turned down in France since the beginning of the year because of a mechanism called the taux d'usure that is in place to stop banks granting loans that are too big for the customer to repay.

The taux d’usure is the maximum rate at which a loan can be granted. It is in place to regulate interest rates and to protect borrowers from taking loans or mortgages that could leave them in financial difficulty.

It is set each quarter by the Banque de France as a percentage.

When a potential buyer goes to a bank to ask for a mortgage, the bank will calculate the annual percentage rate of charge (APRC) of a loan, which includes the basic interest rate as well as loan insurance payments, premiums and other fees.

This APRC of a loan cannot exceed the taux d’usure, which has fixed values set as percentages.

But this year 45% of mortgage applications have been turned down because of this taux d’usure, a new study commissioned by an association grouping financial intermediaries, the Association Française des Intermédiaires Bancaires (AFIB), shows.

“The matter is rather serious," Jérôme Cusanno, head of AFIB, told Franceinfo.

“Our fear is that the entire real estate ecosystem, all the professions and employees, will be impacted by this taux d’usure problem if it is not remedied quickly.”

The study found that of the mortgage refusals, 51% concerned people aged 30 to 55.

Mr Cusanno proposed several solutions to solve the issue, such as overhauling how the taux d’usure is calculated so that it can be increased, removing mortgage insurance payments from the APR calculation, or having the Banque de France step in and increase the taux d’usure for the next month.

The Banque de France increased the taux d’usure on July 1. For 20-year mortgages, it went up from 2.4% to 2.57% and in some cases 2.6%. For mortgages of 10 to 20 years, the rates increased from 2.43% to 2.6% or in some cases 2.63%.

AFIB has called these increases “insufficient”.

Mr Cusanno said that for anyone looking to buy property right now with a mortgage, he recommends holding off.

Landlord in dispute with over unpaid rent removes property’s windows

A landlord is locked in a dispute with an association that provides housing to the elderly and vulnerable, with the association refusing to pay rent until certain renovations are carried out.

Guillaume Steinmetz agreed in December 2021 to rent out his property in Forbach (Moselle) for €950 per month, with the first month free, to the association AMLI.

But he says he “has not received a single penny for eight months”.

“I have contacted all the services, including those of the state, which subsidises the association, but nothing has been done. My demands for payment are all contested. As a result, the eviction procedure is constantly being postponed,” he said.

AMLI does not deny not paying the rent but says that it refuses to do so until necessary renovation work is carried out at the property. This includes installing a safety railing and replacing the windows.

A spokesperson for the association said:

“We are not bad tenants but necessary work needs to be done. We are within our rights. A procedure is underway, the courts will decide.”

Mr Steinmetz has said that work has already been done to the roof and the heating system. He has also taken out the windows in the property and replaced them with wooden panels while waiting on a delivery of new ones.

One tenant is currently living in the property and Mr Steinmetz said that the window to their room has not been removed.

“I didn’t think an association in the field of social care could have such a bad attitude,” he said.

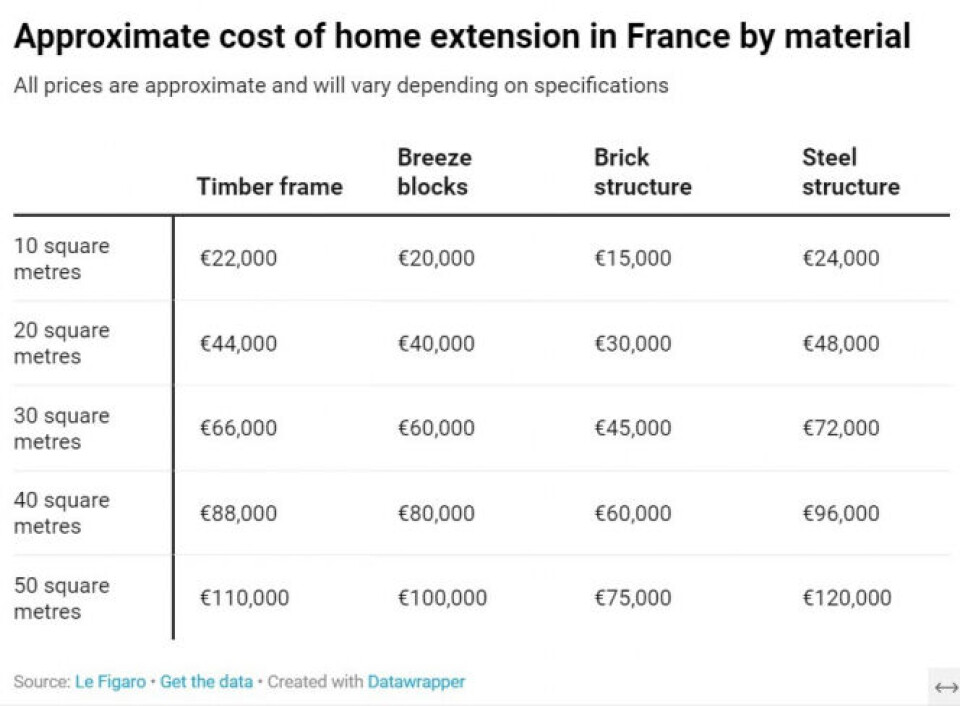

Approximate cost of a home extension

Expanding your house is often an expensive job but that cost depends, of course, on what work you decide to carry out, the materials you use and the size of the extension.

The price often puts people off even thinking about getting the work done. Our table below gives you an idea of how much an extension may cost in France, with the data provided by Le Figaro.

These figures are just averages and the price can vary significantly depending on the specifics, for example the foundations of your property, whether you also want to install a bathroom, the shape of the roof (flat roofs are cheaper), etc. The table is simply a starting point so you can decide if it is worth moving forward and getting a quote for a job.